CommScope Holdings Company, Inc. COMM has gained 315.5% over the past year compared with the Communication Infrastructure industry’s growth of 119.2%. The stock has also outperformed the Zacks Computer & Technology sector and the S&P 500’s growth during this period.

Image Source: Zacks Investment Research

It has also outperformed its competitors, such as Corning Incorporated GLW and Amphenol Corporation APH. Corning has surged 60.2% while Amphenol has gained 61.4% in the past year.

COMM Gains From Product Innovation, Client-Focused Approach

CommScope has been steadily investing in research and development to foster product innovation and reduce the total cost of ownership and deployment of communication infrastructure. The company recently demonstrated record-breaking downstream speeds in a DOCSIS 4.0 network. During the test, a staggering 16.25 Gbps downstream speed across two load-balanced DOCSIS 4.0 modems was achieved, while a single DOCSIS 4.0 modem delivered 9.4+ Gbps downstream speed. Such high speed, comparable to FTTH (Fiber to the Home) on a DOCSIS 4, is of major significance.

FTTH deployment require high upfront investment, the recent breakthrough from CommScope will allow customer to retrieve maximum performance from their existing DOCSIS 4 infrastructure. This initiative is expected to boost CommScope’s prospects in the Access Network Solutions (ANS) segment.

Understanding market trends and developing strong customer relationships are helping CommScope build tailored data and video networking solutions. It is steadily expanding its market presence with service providers outside of North America. The company is effectively identifying underpenetrated metropolitan areas to expand Enterprise sales coverage. It is also investing in capacity expansion to match the demand for products with a high backlog.

The company is benefiting from substantial sales growth in the Access Network Solutions segment. During the second quarter, the ANS segment generated $322 million in net sales compared to $195 million in the year-ago quarter. The 65% year-over-year growth was backed by high demand for DOCSIS 4.0 products and higher license sales. The Connectivity and Cable Solutions segment also benefited from strong cloud and datacenter growth, including GenAI projects.

COMM Rides on Portfolio Optimization

Management’s strategy to optimize the portfolio in alignment with changing market dynamics is a tailwind. It has divested its Outdoor Wireless Networks (OWN) segment in early 2025. It has also inked a definitive agreement with Amphenol Corporation to divest its Connectivity and Cable Solutions Segment for $10.5 billion. The net proceeds will allow COMM to pay off debt, improve liquidity and better equip the company to compete against other industry leaders such as Corning, Cisco, HPE and others.

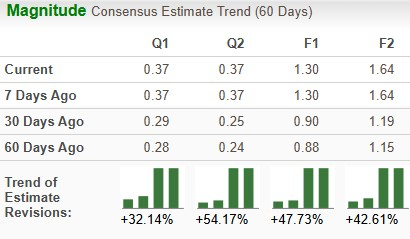

Estimate Revision Trend of COMM

COMM is currently witnessing an uptrend in estimate revisions. Earnings estimates for 2025 have jumped 47.73% to $1.3 over the past 60 days, while the same for 2026 has increased 42.61% to $1.64.

Image Source: Zacks Investment Research

Key Valuation Metric of COMM

From a valuation standpoint, COMM appears to be relatively cheaper compared to the industry but above its mean. Going by the price/sales ratio, the company shares currently trade at 0.63 forward sales, lower than 0.95 for the industry but above its mean of 0.25.

Image Source: Zacks Investment Research

End Note

CommScope is expected to benefit from solid demand trends in the communication infrastructure market. A comprehensive patent portfolio and a strong focus on research and innovation are positive factors. Management’s strategy of boosting liquidity and optimizing portfolio through strategic divestiture will likely drive greater value to shareholders. The positive estimate revision portrays bullish sentiments about the stock’s growth potential. The company currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amphenol Corporation (APH) : Free Stock Analysis Report

Corning Incorporated (GLW) : Free Stock Analysis Report

CommScope Holding Company, Inc. (COMM) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}