The stock market is the only market in the world like it.

In the stock market, lower prices engender pessimism, and higher prices engender optimism.

People chase stocks when they get more expensive, and they run away from stocks when they’re on sale.

It’s easy for even the layman to see how this behavior is counterproductive.

So how do we avoid it?

Well, I’d argue the dividend growth investing strategy is the perfect way to avoid this destructive mentality.

This strategy is all about buying and holding shares in high-quality businesses paying shareholders reliable, rising cash dividend payments.

You can find hundreds of examples by pulling up the Dividend Champions, Contenders, and Challengers list – a compilation of invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

There are two big reasons why this strategy allows one to invest in a “counter cyclical” way, relative to the cycles that plague most investors.

First, there are those wonderful dividends.

When you’re investing so as to increase your dividend income (which can be the bedrock of your eventual financial freedom), you only get more excited when stocks fall and yields rise.

This is a pattern that’s played out for me as I’ve gone about building the FIRE Fund over the last 15 years.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

In fact, I’ve been able to live off of this totally passive dividend income since I quit my job and retired in my early 30s.

How was I able to retire so early in life?

Well, that’s detailed in my Early Retirement Blueprint.

Besides the dividends, there’s another big reason why the dividend growth investing strategy is so effective when it comes to proper investing behavior: valuation.

See, price is just what you pay, but it’s value that you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

By utilizing the dividend growth investing strategy, which naturally encourages investing when valuations are lower and yields are higher, investors can avoid harmful behavior, build wealth, grow passive dividend income, and become financially free in time.

Now, the whole topic of valuation may seem daunting to the uninitiated.

If that’s the case for you, be sure to read Lesson 11: Valuation.

Written by fellow contributor Dave Van Knapp as part of an overarching series of “lessons” designed to teach the dividend growth investing strategy, it provides a quick overview of what valuation, how it works, and how to apply simple tools on your own.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

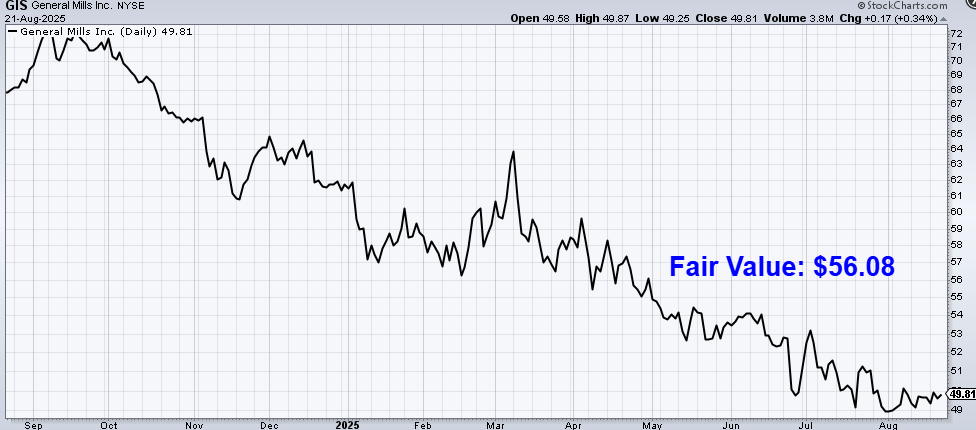

General Mills, Inc. (GIS)

General Mills, Inc. (GIS) is an American multinational manufacturer and marketer of branded, packaged consumer foods and pet foods.

Founded in 1928 (but with roots dating back to 1856), General Mills is now a $27 billion (by market cap) food giant that employs more than 30,000 people.

The company reports revenue across four operating segments: North America Retail, 63% of FY 2024 sales; International, 14%; Pet, 12%; and North America Foodservice, 11%.

As you can see, the vast majority of the company’s revenue is derived from North America.

By product category, Snacks are the company’s largest source of sales (making up about 22% of annual revenue), while Cereal (16%) and Pet (12%) are also major contributors.

On one hand, General Mills is in a tough spot.

It’s a purveyor of packaged and processed foods which have been out of favor for years.

Evolving consumer tastes, trends, and behaviors have tilted the tables toward newer, more agile businesses in the space that provide healthier and more natural options in the marketplace.

Cereal, for instance, has been steadily declining in popularity as a breakfast food (per Euromonitor, cereal market volumes have shrunk roughly two percentage points per year over the past decade) as healthier, protein-forward options have come to the forefront.

On the other hand, the company is still a very profitable enterprise commanding a range of extremely successful, well-known brands such as Cheerios, Häagen-Dazs (in certain markets), Nature Valley, and Pillsbury.

With more than 100 brands in 100 countries, General Mills is one of the world’s foremost packaged food companies, giving it scale, breadth, and leadership that few can rival.

In addition, through a series of acquisitions, the company has pivoted to pet foods, which is an attractive area to be in due to growing ownership and “humanization” of pets.

The company’s Blue Buffalo brand, which is one of the top 10 pet food brands in the US, is especially formidable in this space.

Look, people have to eat.

And while some people would, in a perfect world, prefer to eat healthier meals, these meals can oftentimes be more expensive and time consuming to acquire and/or prepare.

This makes cheaper, more convenient food options an easy choice to make for many consumers in many real-life scenarios.

This is particularly true in the current environment, where high inflation over the last several years has caused food prices to spike, pressuring consumers’ wallets and making cheaper food alternatives more alluring on a relative basis (even if these cheaper options aren’t always healthier choices).

General Mills isn’t growing super quickly.

But it is a stable company that’s been around for more than a century, and there’s no reason to believe it won’t be around for another century.

Along the way, it should continue to consistently grow its revenue, profit, and dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

To that point, General Mills has already increased its dividend for six consecutive years.

Its dividend growth track record would be much more impressive if not for the company’s decision to keep its dividend static for a few years after acquiring Blue Buffalo (an ~$8 billion acquisition which was mostly funded by debt) in order to better manage its cash flow and debt.

The company hasn’t always been super consistent when it comes to dividend increases, but it has been an ultra-reliable dividend star for nearly 130 years: General Mills and its predecessor company have been paying uninterrupted dividends since 1898.

For dividend lovers, that’s music to the ear.

The temporary halt to dividend growth (but not to steady dividend payments) was, arguably, for the better, putting the company on better long-term financial footing.

Putting that aside, the three-year dividend growth rate of 5.3% is fairly solid.

No, it’s not lighting the world on fire.

However, this is getting layered on top of the stock’s market-smashing yield of 4.9%.

That yield is in territory usually reserved for yield plays such as REITs and utilities.

It’s pretty surprising to see a staid food company competing with REITs on yield.

For better perspective, this yield is 140 basis points higher than its own five-year average.

An incredible spread.

And with the payout ratio sitting at 58%, this dividend looks quite safe.

The yield being so unusually high makes this a compelling option for income-seeking investors who aren’t necessarily in the market for fast growth.

Many 5% yields out there come with even lower growth than this, so one isn’t really making some big sacrifice here.

I think this is one of the better and more sustainable 5% yields in the market.

Revenue and Earnings Growth

As much as that may be true, though, these metrics are mainly based on what’s already happened in the past.

However, investors must always be thinking about what could happen in the future, as today’s capital is risked for tomorrow’s rewards.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will be of use when estimating fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this way should give us what we need to roughly judge where the business might be going from here.

General Mills grew its revenue from $16.6 billion in FY 2016 to $19.5 billion in FY 2025.

That’s a compound annual growth rate of 1.8%.

Somewhat disappointing, although this isn’t shocking.

We’re talking about a mature, staid company fighting a secular shift away from packaged, processed foods.

What’s a bit disappointing here, though, is the fact that this even includes the large Blue Buffalo acquisition, meaning we’d be looking at even worse figure if not for the foray into pet foods.

Meantime, earnings per share increased from $2.77 to $4.10 over this period, which is a CAGR of 4.5%.

A combination of buybacks and margin expansion helped to drive excess bottom-line growth.

Regarding the former, the outstanding share count has been reduced by ~9% over the last decade.

Expanding margins and steady buybacks indicate to me that management has done an admirable job of steering the company in the face of challenging industry trends and macroeconomics.

It’s not like management is resting on their laurels and/or actively trying to ruin the company.

There have been incremental changes in the portfolio, along with acquisitions designed to better suit the marketplace.

Looking forward, CFRA believes that General Mills will put up a -4% CAGR in EPS over the next three years.

Regarding the pessimism, CFRA cites: “…weak organic growth across key categories due to value-seeking consumers, shifting consumer habits, and heightened competition from branded players and private labels.”

I don’t think CFRA is totally out of line here.

General Mills most recently reported a 2% decrease in revenue and 5% decrease in EPS for Q4 FY 2025.

A tumultuous period during the pandemic, which resulted in lumpy demand and high inflation/input costs, led companies like General Mills to sacrifice volumes in order to take price and maintain margins.

If there is a knock against management, it may be the long-term give on volumes in order to take short-term gains on pricing.

In my view, this was a mistake that gave private labels an advantage (which may be permanent in nature).

Things are still in the process of normalizing for General Mills, and Q4’s numbers were an improvement showing the company moving in the right direction, but we’re not totally there yet.

A continued slow descent into deterioration and mediocrity over the coming years would be undoubtedly a disappointing outcome for shareholders, even with the dividend.

After all, 4% shrinkage is barely offset by a 5% yield, and the stock’s 1.9% CAGR (including reinvested dividends) over the last decade is quite poor and goes to show the importance of total return.

Those who have held this stock over the last decade have little to show for their patience and would have done much better had they instead held shares in any number of higher-quality businesses.

Of course, that’s the past.

What matters now is the future.

On this front, I’m not quite as negative as CFRA, and I do think a normalization process, which is clearly playing out in the numbers, gives us something to be optimistic about directionally.

All General Mills has to do is grow the business at a low-single-digit rate (which opens the dividend up for like-or-better growth) in order to be a satisfactory investment from here.

It’s not a high hurdle to clear.

As Warren Buffett might say, this is a one-foot bar to step over.

General Mills increased its dividend by 1.7% in June, and this is during a time which is about as bad as it gets for the company.

Even modest improvement can get the dividend growth back into a mid-single-digit range, which would be more than enough to make sense of a stock already yielding 5%.

If one leans toward yield/income, this all adds up to something pretty interesting.

Financial Position

Moving over to the balance sheet, General Mills has a decent financial position.

The long-term debt/equity ratio is 1.4, while the interest coverage ratio is just over 6.

These numbers aren’t awful, but they’re also nothing to write home about.

While General Mills has never (for as long as I’ve been investing) had anything close to a pristine balance sheet, its financial position has weakened in recent years (most notably from the large Blue Buffalo acquisition).

I’d like to see some improvement here, but industry dynamics will likely limit any possibility of material movement.

Profitability is fairly robust.

Return on equity has averaged 25.7% over the last five years, while net margin has averaged 12.9%.

Surprisingly strong numbers.

ROE is juiced by the balance sheet, but even ROIC is routinely in a low-double-digit range.

General Mills has seen better days, but it remains a top-tier company in its space (as challenged as that space may be).

And with economies of scale, brand/pricing power, established retail shelf space, and a global distribution network, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Competition, in particular, is a problem – a multifaceted problem, no less – as General Mills faces competition from traditional players, retailers (via private-label products), and newer entrants resonating with younger consumers.

Adding on to that prior risk factor, the company’s major direct customers (i.e., retailers) have increasingly become competitors (by selling their own private-label products).

There is a secular shift away from a large portion of the company’s products.

The current US presidential administration has apparently taken a harsh stance toward packaged/processed foods, which is a headwind for General Mills.

Recent price taking has hurt volumes, and this short-term gain for long-term pain may be permanent for General Mills.

The stretched balance sheet limits M&A opportunities, which has recently been one of the only ways in which General Mills has been able to adapt to changing trends.

Input costs vary.

Being a global company, General Mills is exposed to currency exchange rates, different/changing tastes across cultures, and geopolitics.

The rise of GLP-1s may accelerate the secular shift away from processed foods.

I definitely see some risks to contend with.

However, the market has already sniffed these risks out and reassigned the stock an extremely low valuation after a 45% drop in the stock’s price since May 2023…

Valuation

The P/E ratio is 12.1.

Yes, just 12.1.

Even for a company that’s seen better days, that is shockingly low (especially in this market).

To be fair, this stock has rarely commanded high multiples, but this current P/E ratio is well below its own five-year average of 15.8.

The P/CF ratio of 10.2, which is very undemanding, is also far lower than its own five-year average of 12.9.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 5%.

I’m basically assuming that General Mills can get back to something it’s historically been close to.

This would only require low-single-digit top-line growth, upon which General Mills can pull some levers (such as buybacks and margin expansion) to get EPS to a mid-single-digit type of growth rate.

That would allow the dividend to cruise along at a 5% or so growth rate.

There’s nothing herculean about that, but General Mills will have to tweak the portfolio and continue to respond to changing dynamics across the marketplace.

The DDM analysis gives me a fair value of $51.24.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

From my vantage point, the stock looks slightly better than fairly valued after a heavy beatdown and revaluation by the market.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates GIS as a 4-star stock, with a fair value estimate of $62.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates GIS as a 3-star “HOLD”, with a 12-month target price of $55.00.

I’m on the low end this time around. Averaging the three numbers out gives us a final valuation of $56.08, which would indicate the stock is possibly 11% undervalued.

Bottom line: General Mills, Inc. (GIS), with more than 100 brands in more than 100 countries, is one of the world’s foremost packaged food companies. Despite challenging dynamics in its industry, General Mills has scale, breadth, and leadership that few can rival. With a market-smashing yield, mid-single-digit dividend growth, a reasonable payout ratio, more than five consecutive years of dividend increases, and the potential that shares 11% undervalued, income-leaning, value-seeking dividend growth investors have a cheap, high-yield stock on their hands here.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is GIS’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 90. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, GIS’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Disclosure: I’m long GIS.

{kind=link}