How many things are truly “great” in life – especially in any one category?

How many truly great humans have ever lived out of 100+ billion that have come and gone?

History only remembers a small portion of all people to ever be born.

Are there really that many great experiences you’ve had in your life, or have they been limited to a handful of memories that you can easily recount because they stand out so much (due to how great they were)?

Greatness is, in my experience, actually quite rare.

Not everything can even be above average (or there would be no average), let alone great.

And this certainly is true for businesses.

Out of the ~60,000 publicly-traded companies in the world, likely less than 10% are actually great businesses.

But how do you go about finding these gems?

Well, a good place to start is the Dividend Champions, Contenders, and Challengers list, which has pulled together important data on hundreds of US-listed stocks have have raised dividends each year for at least the last five consecutive years.

This list acts as a filter, excluding all companies that either don’t pay dividends (which could indicate a lack of profit necessary to afford dividends) or can’t grow dividends (which could indicate a lack of growth necessary to sustain growing dividends).

All stocks on that list qualify for the dividend growth investing strategy – a long-term strategy whereby one buys and holds shares in great businesses that prove their greatness by rewarding shareholders with steadily rising cash dividend payouts.

A growing dividend isn’t an automatic signal that a business is great, but it sure is a pretty good starting point to research further.

I’ve used the dividend growth investing strategy over the last 15+ years to build the FIRE Fund.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

This allowed me to quit my job and retire in my early 30s.

If you’re interested in doing the same, be sure to read my Early Retirement Blueprint.

As critical as it is to invest in great businesses, it’s arguably just as critical to invest when the valuation is great.

And that’s because price is only what you pay, but value is what you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Combining great businesses with great valuations by steadily buying undervalued high-quality dividend growth stocks can lead to fabulous levels of wealth, passive dividend income, and freedom over time.

Now, spotting and taking advantage of great valuations does require one to already be familiar with the concept of valuation.

If that familiarity isn’t already in place for you, that’s where Lesson 11: Valuation comes in handy.

Written by fellow contributor Dave Van Knapp, it explains the ins and outs of valuation using very simple terminology and helps to familiarize anyone with what valuation is and how to apply it.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Pentair PLC (PNR)

Pentair PLC (PNR) is an American global water treatment company.

Founded in 1966, Pentair is now a $14 billion (by market cap) water treatment solutions leader employing 9,000 people.

The company reports results across three segments: Pool, 38% of FY 2025 sales; Flow, 37%; and Water Solutions, 25%.

Pentair manufactures a range of water treatment solution products for a variety of end uses, including filtration systems, pressure tanks, pumps, and spray nozzles.

As I’ve stated before, I think clean, usable, accessible water will be the “liquid gold” of the coming century, just as oil has been for the last century.

Water is our most precious resource.

While we cannot viably have a modern-day society without petroleum, we literally cannot survive without water.

This level of necessity puts companies that facilitate the accessibility and usability of clean water in an extremely favorable position over the coming years.

Pentair is one such company.

Moreover, being a global leader in this area, Pentair stands to disproportionately benefit from these secular growth dynamics.

And that’s what puts it in a fantastic spot as it relates to being able to continue growing its revenue, profit, and dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

Already, Pentair is an absolute legend when it comes to reliable dividend growth.

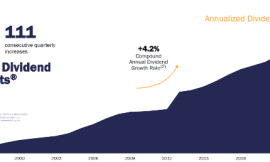

The company has increased its dividend for 50 consecutive years – a newly-crowned Dividend King.

However, because of a massive spin-off of its electric business via nVent Electric PLC (NVT) in 2018, its dividend growth rate over the last decade has fluctuated quite a bit.

Zooming on more recent dividend growth, which reflects the pure-play Pentair that exists now, we can see a three-year dividend growth rate of 6%.

And the last two dividend raises came in at 8% or higher.

I think this high-single-digit dividend growth of late gives us a good read on what Pentair is capable of and likely will deliver on a go-forward basis.

With a payout ratio of only 27.3%, there’s certainly plenty of headroom to move the dividend meaningfully higher.

However, the trade-off one has to make in this case, which is common across the entire water theme broadly, is current yield.

Because of the appeal of secular growth within this space, a lot of stocks with a strong attachment to almost anything related water tend to have high market demand, pushing yields down.

To that point, this stock’s yield is only 1.3%.

This yield is in line with its own five-year average, meaning this is what the market has been willing to accept from this stock.

Those who are more in need of current income (such as retirees) will find this yield problematic.

But if one has a long time horizon and can allow the compounding process to play out, they’ll likely look at the long-term potential and like what they see.

Revenue and Earnings Growth

As likable as all of that may be, though, the dividend metrics are mainly based on what’s already happened.

However, investors must always be thinking what’s yet to occur, as the capital of today is risked for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be of aid during the valuation process.

I’ll first show you what the business has done over the last seven years in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this way should give us a baseline understanding of where the business could be going from here.

While I usually show a decade’s worth of growth, I’m only using seven years in this case because that aforementioned 2018 spin-off of nVent had a major impact on Pentair’s financials.

Pentair grew its revenue from $3 billion in FY 2019 to $4.2 billion in FY 2025.

That’s a compound annual growth rate of 5.8%.

That’s a solid rate of top-line growth from a large, mature company that spun out a very dynamic portion of its business.

Notably, nVent Electric’s market cap of $19 billion actually exceeds that of Pentair by a healthy margin.

Just imagine what a still-combined company could have done!

Meanwhile, earnings per share increased from $2.09 to $3.96 over this period, which is a CAGR of 11.2%.

For Pentair to do this after losing a world-class operation is awfully impressive and showcases the strength of the business model and the power of secular growth within water-related solutions.

Looking forward, CFRA is projecting a 9% compound annual growth rate for Pentair’s EPS over the next three years.

Rising CapEx across municipalities relating to strict new standards around PFAS is a huge catalyst for Pentair.

Water utilities left and right are spending big on water treatment, and Pentair is an obvious beneficiary of this.

And that’s on top of the healthy filtration demand from residential and commercial customers.

Plus, there’s the large pool business that takes advantage of a huge installed base with captive customers whereby sensitive and proprietary components need intermittent replacement (and no rational customer is going to risk a very expensive pool in order to save a few bucks on maintenance).

This EPS growth forecast looks quite reasonable to me, and it builds in a scenario where low-double-digit dividend growth is affordable and realistic over the near term (by virtue of the low payout ratio).

Pairing that with the starting yield gets one to a low-teens type of annualized total return setup from here, assuming no change in multiples.

Getting that on a Dividend King with incredible revenue visibility and secular growth is obviously very appealing.

Financial Position

Moving over to the balance sheet, Pentair has a very good financial position.

The long-term debt/equity ratio is 0.4, while the interest coverage ratio is 12.

The long-term debt load of about $1.6 billion is not egregious or cumbersome for a company of this size.

Pentair has investment-grade credit rating (albeit on the low end): Baa3, Moody’s; BBB-, S&P.

Profitability is robust.

Return on equity has averaged 20.1% over the last five years, while net margin has averaged 14.5%.

These are very solid numbers, indicating strong margins and high returns on capital.

This is a terrific business in a terrific space.

And with economies of scale, switching costs, a reputation for quality/reliability regarding mission-critical products, IP, and a large installed base requiring replacement parts, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Relative to other business models, however, I see all three as being somewhat diminished for Pentair.

And regulation can actually help Pentair more than hurting it, as strict regulation regarding water treatment (such as new PFAS drinking water water standards) are requiring massive municipal investments in water infrastructure (which will almost certainly be supportive of Pentair).

Being an international company, Pentair is exposed to geopolitics and currency exchange rates.

Pentair can exhibit cyclicality, particularly in relation to infrastructure components in new builds.

Nearly 40% of Pentair’s revenue comes from the Pool segment, and spending on pools is highly discretionary.

Pentair has long had a more diversified business model that could lean on different strengths at different times, but its major 2018 spin-off of nVent Electric has made Pentair much more concentrated as a pure-play water company.

Overall, I don’t consider Pentair to be an especially risky type of business, and that easier risk profile has long made it acceptable for the stock to command high multiples.

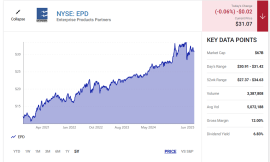

However, a recent 20% pullback in the stock’s pricing has resulted in those multiples being fairly reasonable…

Valuation

The P/E ratio, based on adjusted EPS, is 18.4.

That is not high for a water company reliably growing at HSD-LDD rates.

This stock often commands a P/E ratio north of 25.

The cash flow multiple of 17.2 is also very reasonable, and it’s below its own five-year average of 17.6.

And the yield, as noted earlier, is in line with its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 10-year dividend growth rate of 13%, and a long-term dividend growth rate of 8%.

The near-term portion of the model reflects Pentair’s recent acceleration in the rate of its dividend growth, although I’m extrapolating that out in a way that assumes even more acceleration.

Seeing EPS growth where it’s at (both what’s been demonstrated and what’s forecasted ahead), and with the payout ratio being as low as it is, Pentair seems fully capable of doing a low-teens type of dividend growth rate over the next several years.

I would then expect that to naturally slow down into a high-single-digit range befitting of a mature company.

The DDM analysis gives me a fair value of $88.89.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

From my vantage point, this stock is, at worst, fairly valued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates PNR as a 3-star stock, with a fair value estimate of $97.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates PNR as a 4-star “BUY” with a 12-month target price of $130.00.

I’m surprised to see that I came out so low. Averaging the three numbers out gives us a final valuation of $105.30, which would indicate the stock is possibly 14% undervalued.

Bottom line: Pentair PLC (PNR) is a high-quality company operating in one of the most attractive areas of the global economy. It caters to humanity’s most precious resource and what is likely going to be the “liquid gold” of the coming century. With a market-beating yield, high-single-digit dividend growth, a low payout ratio, 50 consecutive years of dividend increases, and the potential that shares are 14% undervalued, this Dividend King could be one of the best ways for long-term dividend growth investors to play the secular growth theme in water.

-Jason Fieber

Note from D&I: How safe is PNR‘s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 89. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, PNR’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Disclosure: I have no position in PNR.

{kind=link}