Last summer, I had lunch with my friend and colleague Dave Van Knapp, and I shared something with him that I haven’t told very many people: Starting in late 2022 and continuing throughout the majority of 2023, I sold almost all the income-generating assets in my primary brokerage account.

That included everything from dividend growth stocks I thought I’d hold forever … to my favorite high-yield, tax-advantaged funds that paid monthly.

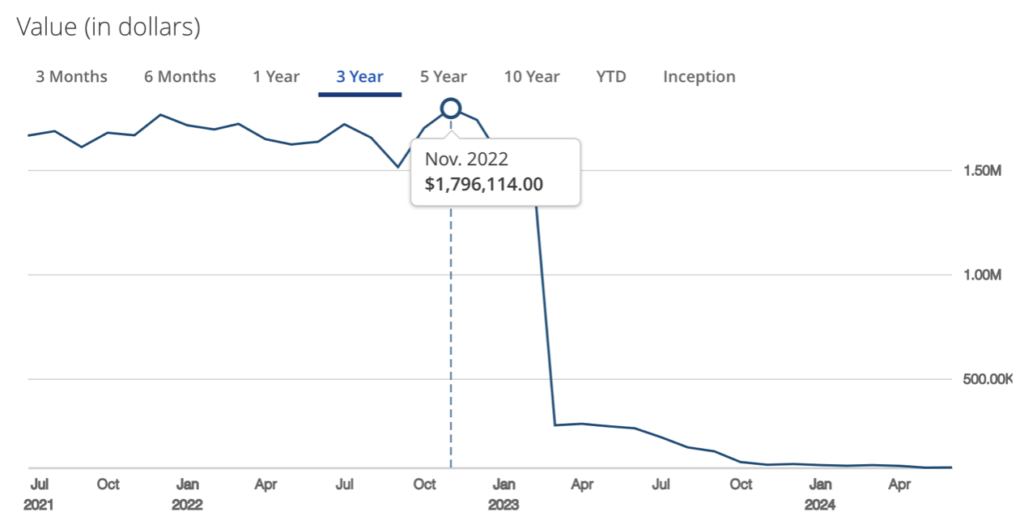

You can see the change in my portfolio’s total value below. The portfolio had peaked around $1.8 million in November 2022 shortly before I started to sell.

Needless to say, I took a massive pay cut.

From the peak, this portfolio went from generating around $5,000-$6,000/month in reliable dividend income to around $120/month today (or $1,437/year). It’s currently valued at just over $75,000.

To rub salt into the wound, take a look at what the market has done since I first started liquidating this portfolio at the end of 2022. Stocks are up around 80%.

If I had stayed vested in the market, my $1.8 million portfolio would likely be worth around $3.2 million today. More meaningful than that, though, consider this: At the current 4.0% rate, putting that $3.2 million in a 10-year Treasury note could generate the equivalent of a guaranteed, risk-free $10,667/month for the next decade.

When that note matures in 2036, I’d only have another 3.5 years until I’d be eligible to start pulling penalty-free income from my 401(k), which holds a combination of dividend stocks and option income plays. I’d also likely convert the holdings in my Roth IRA, which is concentrated on growth stocks, into income-producing securities.

Alas… it could have been smooth sailing into retirement, if only I would have stayed vested!

Which begs the question: Why would I sell out of such a relatively large, passive income stream in the first place? Where did the money go?

The answer my surprise you. I’ll share the details next time… and let you know if I have any regrets.

Good investing!

Greg Patrick

{kind=link}