Net worth is cool.

But you know what’s cooler?

Cash flow.

And that’s because we don’t go and buy things down at the “net worth store”.

Instead, ongoing expenses get covered with ongoing cash flow.

This is just one of many reasons why I’m a big fan of dividend growth investing, which is a long-term investment strategy involving the buying and holding of shares in terrific businesses paying reliable, rising dividends to shareholders.

You can find hundreds of examples of these businesses by taking a look at the Dividend Champions, Contenders, and Challengers list, which has invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Those cash dividends are at the heart of the story here.

Rather than converting net worth to cash flow by selling off holdings, owning stock in companies paying dividends quite literally allows you to have your cake and also eat it (by collecting cash flow from stock holdings while also retaining those stock holdings in full).

And when those dividends are also steadily growing, you get to fight off inflation and become almost financially bulletproof.

I’ve used this methodology over the last 15 years to build the FIRE Fund.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

It’s actually been enough to cover my simple lifestyle since I quit my job and retired in my early 30s.

For more details on how such an early retirement is possible, check out my Early Retirement Blueprint.

Buying stock in great businesses paying out safe, growing dividends is a big part of all of this, but buying at the right valuations is also of critical importance.

See, price only tells you what you pay, but value tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Focusing on cash flow, rather than net worth, by systematically buying and holding undervalued high-quality dividend growth stocks can get almost anyone to a position of financial independence and even a very early retirement.

Of course, the whole notion of recognizing undervaluation means one already understands how valuation works.

Well, that’s where Lesson 11: Valuation comes in.

Written by fellow contributor Dave Van Knapp, it shares the ins and outs of valuation using simple terminology, even providing a template you can go off and easily use on your own.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

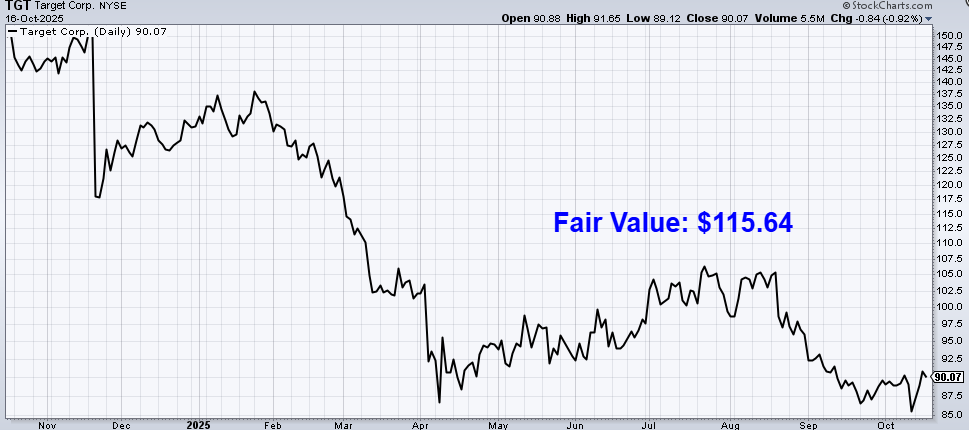

Target Corp. (TGT)

Target Corp. (TGT) is an American big-box retailer.

Founded in 1902, Target is now a $39 billion (by market cap) retail giant that employs almost 450,000 people.

Target operates nearly 2,000 stores, and it has a footprint across all 50 states.

By revenue, Target was recently ranked as the seventh-largest retailer in the US.

Target has long targeted (pun not intended) an upgraded shopping experience, giving its stores an elevated look and feel in terms of design, merchandise, and service.

Yet, it simultaneously threaded the needle on pricing, still providing good value for money by offering affordable products.

Striking a deft balance between stylish quality and everyday value gave the retailer a “cheap chic” reputation, leading to the infamous “Tarzhay” moniker (a playful mock-French pronunciation of Target to make it sound fancy).

However, in the last few years, numerous missteps, ranging from visible political statements to poor inventory management, have led to well-publicized struggles at the once-mighty retailer.

That said, “struggling” may be a bit of an exaggeration, with numerous fundamental metrics not all that far of from all-time highs.

On the other hand, the stock is way off of all-time highs, leading to, perhaps, more value in the shares than at the stores.

Moreover, many of the self-inflicted wounds are rather temporary and very fixable.

Despite some shine recently coming off of the retailer, Target remains a household name where millions of Americans still repeatedly buy everyday goods, setting up the company for continued revenue, profit, and dividend growth in the years ahead.

Dividend Growth, Growth Rate, Payout Ratio and Yield

To date, Target has increased its dividend for 58 consecutive years.

That easily qualifies Target for its status as a vaunted Dividend Aristocrat.

It’s actually nearly a Dividend Aristocrat twice over – an incredible feat, showing a rare level of consistency.

This tells us that Target has been here before.

It’s faced challenges and changes over the decades, and it’s obviously navigated through all of that just fine (or else it wouldn’t have been able to increase its dividend for almost 60 straight years).

Its 10-year dividend growth rate of 8.9% is very strong, especially for a mature retailer (Target was already 110+ years old a decade ago), but more recent dividend growth has reflected difficulties and been in a low-single-digit range.

Obviously, it would be unreasonable to expect a constant dividend growth rate from any company, as business conditions are never static, but this slowdown has been dramatic.

At the same time, the stock’s yield has shot much higher, compensating new investors for that drop in dividend growth (which could be a temporary drop anyhow).

The stock is now yielding a jaw-dropping 5.2%.

This market-smashing yield is 300 basis points higher than its own five-year average.

It’s an incredible spread.

And while the dividend growth slowdown may be a temporary blip, this higher-than-average yield gets to be “locked in” by those buying in now.

Providing an extra sigh of relief around the dividend is the payout ratio, which is only 53.1%.

That’s a very healthy payout ratio.

It’s unusual to see a payout ratio this low when a yield is this high, as high yields are often accompanied by high payout ratios.

To me, this all looks like a very advantageous setup for long-term investors able to courageously go against the crowd.

The anomalous nature of all of this is quite appealing.

Revenue and Earnings Growth

As appealing as it may be, though, this dividend profile is largely based on preceding data.

However, investors must always be thinking about possible forthcoming events, as today’s capital is risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be of use during the valuation process.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this way should give us a baseline upon which to roughly judge where the business could be going from here.

Target moved its revenue from $73.8 billion in FY 2016 to $106.6 billion in FY 2025.

That’s a compound annual growth rate of 4.2%.

Respectable.

I’d usually expect mid-single-digit top-line growth out of a business like this, and Target is, well, right on target.

Meanwhile, the company increased its earnings per share from $5.31 to $8.86 over this period, which is a CAGR of 5.9%.

A 25%+ drop in the outstanding share count, powered by steady buybacks, drove this excess bottom-line growth.

Again, it’s respectable.

It would have looked a lot better than respectable – closer to something amazing – if we had done this 10-year look-back just three years ago, but a post-pandemic correction which was exacerbated by poor inventory management and merchandising has led us to a suboptimal result.

Also, to further contextualize things, what happened here is, there was phenomenal growth between 2020 and 2022 (around the time of the pandemic), and then we followed that up with a big correction in earnings in 2023 (which is not all that unsurprising) and back to growth thereafter.

Still, mid-single-digit growth, even with a very tough stretch thrown into the mix, is really not bad at all when you’re starting off with a 5%+ yield.

From here, that can get one to a 10%+ annualized total return, even without a return to historical growth and/or any return to historical multiples on the stock (which could be “twin engines” driving far higher returns over the coming years, if materialized).

Looking forward, CFRA expects Target to compound its EPS at an annual rate of 1% over the next three years.

To be sure, this is uninspiring, but CFRA does telegraph this as a short-term view against longer-term optimism.

CFRA’s passage here highlights this juxtaposition: “We expect [Target] to return to low-single digit comparable sales growth in FY 27 as it brings more newness and innovation at affordable price points. Focus will be on execution and whether [Target] can bring back its “Tarzhay” magic through improved guest experience. Long-term growth drivers include digital expansion (20% of sales vs. 9% prepandemic) and store expansion (300 new stores over 10 years).”

That digital expansion, aided by services such as free curb-side pickup and its Shipt platform (which offers same-day delivery of Target orders), means this is not the same Target that existed just 10 years ago.

It’s clear that Target is more advanced, nimble, and able to meet the customer wherever they may be.

In addition, Target has been taking a page out of the Amazon.com Inc. (AMZN) playbook by introducing Target Plus (third-party retailing), Target Circle 360 (membership), and Roundel (retail media/advertising).

Target being able to replicate even a tiny portion of Amazon’s success on these fronts can reap big rewards for the firm, particularly since its stock is so much cheaper (which could lead to the needle really moving in terms of a rerating).

On top of all of this, Target’s recent lean into grocery gives it a more repeatable, recurring source of traffic and revenue above and beyond its legacy household merchandise.

While I have no issues with CFRA’s near-term pessimism, longer-term optimism seems warranted here.

Target is largely a self-help story still deeply entrenched in the everyday American experience and psyche – now with grocery, digital, delivery, and advertising to go along with it.

And even while it deals with self-inflicted wounds, we have to keep in mind that its $106.6 billion in revenue last fiscal year isn’t far off from its all-time high of 109.1 billion.

It’s not a totally different operation here.

I don’t see a crisis.

In my view, modest improvements would be all that’s necessary to revive excitement around this idea and get Target back on track as both a business and stock.

And one gets to collect a 5%+ yield while waiting for that to play out.

It’s not a bad setup at all for value-minded, income-leaning investors.

Financial Position

Moving over to the balance sheet, Target has a good financial position.

The long-term debt/equity ratio is 1.0, while the interest coverage ratio is nearly 14.

Its long-term debt has credit ratings well into investment-grade territory: A2, Moody’s; A, Standard & Poor’s.

Its ~$14 billion in long-term debt is not overly material for a company of this size, and its balance sheet has been responsibly managed for many years now.

I see no issues here.

Profitability is strong for a retailer.

Return on equity has averaged 34% over the last five years, while net margin has averaged 4.3%.

ROE is impressive, and ROIC is routinely coming in at around 15%.

Target is generating pretty high returns on capital, which is a lovely sight.

Razor-thin margins are common in retail, so one does have to keep that in mind, but Target’s margins are actually decently strong for a general retailer.

Overall, Target is running a really good business, even though it’s coming off of some recent highs.

And with economies of scale, brand recognition, negotiating power with suppliers, and a private-brand business housed within the retailer, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

While regulation and litigation aren’t major risks for a retailer, this industry is intensely competitive.

Building on that last point, Target is well behind some of its key competitors in terms of scale and growth.

Target’s brand has lost some of its luster in recent years.

Stores are largely dedicated to trendy home goods, which help margins and differentiate Target, but these discretionary products could face pressure in times of economic weakness, meaning Target is less insulated from economic volatility than some of its competitors.

Target’s moves into more grocery help to lessen its reliance on discretionary purchases, but this comes at the cost of lower margins and less differentiation.

Target has tried in the past to expand its footprint internationally, but these efforts have failed thus far, indicating the retailer may have limited growth potential beyond the US (which is already fairly saturated).

Tariffs are a new wrinkle introducing uncertainty around Target’s sales and margins.

I don’t view Target as an overly risky business model, evidenced by its multidecade dividend growth streak.

Yet, with the stock down nearly 70% from 2021 peak, there seems to be an unwarranted amount of risk and uncertainty being priced in right now…

Valuation

The stock is now trading hands for a lowly P/E ratio of 10.2.

That’s well below the stock’s own five-year average P/E ratio of 16.8.

This is also less than half that of the broader market’s earnings multiple.

The cash flow multiple of 5.5, which is astonishingly low in absolute terms, is way lower than its own five-year average of 9.4.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 5.5%.

This is one of the lower dividend growth rates I’ve resorted to, but I think it appropriately balances everything out.

This is roughly right between the 10-year dividend growth rate and more recent dividend growth.

It’s also very close to (but slightly less than) Target’s demonstrated 10-year EPS CAGR, and that’s a period in which the company was not performing optimally.

With Target sporting new growth verticals (such as Target Plus and Roundel), it seems unlikely that EPS (and, thus, dividend) growth over the next decade will come in at less than the last decade (albeit while acknowledging that near-term growth will be limited), which easily opens up room for some upside surprise here.

The DDM analysis gives me a fair value of $106.91.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Even with a pretty conservative valuation model, the stock still looks cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates TGT as a 4-star stock, with a fair value estimate of $123.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates TGT as a 4-star “BUY”, with a 12-month target price of $117.00.

I ended up low, evidently confirming that I did use a conservative model in this case. Averaging the three numbers out gives us a final valuation of $115.64, which would indicate the stock is possibly 24% undervalued.

Bottom line: Target Corp. (TGT) is established in the American consciousness as a go-to retailer, known for its upscale products and shopping experience available at everyday value and affordability. It’s differentiated itself in the marketplace and earned its precious “Tarzhay” moniker. Despite some self-inflicted wounds, only modest improvement is necessary to right the ship, making it an easy self-help story. With more than 50 consecutive years of dividend increases, a balanced payout ratio, a sky-high yield, high-single-digit dividend growth, and the potential that shares are 24% undervalued, this Dividend Aristocrat and soon-to-be Dividend King is low-hanging fruit for long-term dividend growth investors.

-Jason Fieber

Note from D&I: How safe is TGT‘s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 80. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, TGT‘s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Disclosure: I have no position in TGT.

{kind=link}