I’m a fan of hard work.

But guess what?

You can work as hard as you possibly can, but your progress will still be limited.

There’s only so much time in a day.

And a fixed hourly rate is also a big limiting factor.

This is why working smarter, not necessarily harder, is critical to long-term financial success.

The smartest way to work is to have your money work for you.

This is most easily done through investing.

See, money can work 24/7, and it can grow exponentially.

Capital can be a far, far more effective worker than you or I could ever hope to be.

While investing, in general, is a great start, dividend growth investing, in particular, might just be the best way to invest and put your money to work.

This strategy involves buying and holding shares in world-class businesses rewarding shareholders with reliable, rising cash dividends.

Those rising cash dividends are only sustainable over the long run when they’re funded by rising profits, and rising profits tend to only emanate from great businesses.

You can see what I mean by taking a peek at the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Great businesses are often great long-term investments, and being almost automatically restricted to these great investments is at the heart of why dividend growth investing is almost a can’t-lose way to invest.

I’ve been using the strategy for myself for the last 15 years, allowing it to guide me as I’ve gone about building the FIRE Fund.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

This passive dividend income has been enough to cover my basic bills in life ever since I quit my job and retired in my early 30s.

For more on how such an early retirement is possible, be sure to read my Early Retirement Blueprint.

As I said, great businesses often make for great long-term investments, but valuation at the time of making any investment will have a lot to say about one’s results.

That’s because price is only what you pay, but it’s value that you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Working smarter, not harder, by putting your capital to work through the dividend growth investing strategy and steadily buying undervalued high-quality dividend growth stocks is an almost can’t-lose way to build serious wealth, passive dividend income, and independence in your life over time.

But undervaluation is only helpful if one can actually spot it, and that does require one to already understand how valuation works.

For anyone lacking that understanding, Lesson 11: Valuation will help immensely.

Written by fellow contributor Dave Van Knapp as part of a series of “lessons” designed to teach the dividend growth investing strategy, this lesson describes the basics of valuation and shares how to use simple tools to confidently assess the valuation of just about any dividend growth stock you’ll run across.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

A. O. Smith Corp. (AOS)

A. O. Smith Corp. (AOS) is a manufacturer of a broad range of residential and commercial water heaters and boilers, along with water and air purification systems.

Founded in 1874, A. O. Smith is now a $10 billion (by market cap) water technology leader that employs nearly 13,000 people.

The company reports results across two geographic segments: North America, 75% of FY 2024 revenue; and Rest of World, 25%.

One of the biggest challenges facing the world right now is reliable access to clean, usable water.

Water, which is necessary to sustain human life, is our most precious resource; yet, for a variety of reasons, it’s becoming increasingly difficult to get it.

A resource with finite supply has nearly infinite demand, and there’s no future in humans will suddenly stop demanding or requiring clean water.

As oil was the “liquid gold” of the 20th century, water will be for the 21st century.

Thus, companies which provide products and/or services to facilitate the easier and more efficient delivery/usage of clean water stand to do very well.

Through its purification systems and high-tech water heaters, A. O. Smith is one such company.

This is a pure-play water technology company positioned at the center of this secular megatrend, helping to provide both clean water (via purification systems) and more efficient water (via high-tech water heaters).

Its core product, water heaters, have always benefitted from steady demand (since most households are unwilling to live without water heaters), but its newer, higher-tech (i.e., tankless) water heaters are a new growth angle, promising greater efficiency and cost savings over an installation’s lifetime.

Despite being more than 150 years old, A. O. Smith might actually be in the best spot it’s ever been in, being an established, well-regarded, scaled player in an industry seeing an inflection point regarding its supply-demand setup.

And that’s why the coming years auger well for the company’s ability to generate growth across its revenue, profit, and dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

Already, A. O. Smith has increased its dividend for 31 consecutive years.

That easily qualifies it for its status as an esteemed Dividend Aristocrat, and this also goes to show just how consistent and reliable A. O. Smith has been for decades.

Its 10-year dividend growth rate of 15.8% is very strong, but more recent dividend raises have been in a more moderate high-single-digit area.

Still, high-single-digit dividend growth is more than enough to make sense of the stock, as it currently yields 1.9%.

This market-beating yield, by the way, is 20 basis points higher than its own five-year average.

A payout ratio of just 38% also shows us a very safe dividend, poised for much more growth ahead.

With the payout ratio being as low as it is, and with the business growing as steadily as it is, this is a Dividend Aristocrat really just getting started with its dividend growth story.

The yield might be a tad on the low side for those seeking more immediate income, but this is otherwise a fantastic dividend profile.

Revenue and Earnings Growth

As fantastic as it may be, though, this profile is largely based on information from a preceding time.

However, investors must always be thinking about succeeding events, as today’s capital ultimately gets risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful for the valuation process.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this way should give us the ability to judge to a reasonable degree where the business could be going from here.

A. O. Smith advanced its revenue from $2.5 billion in FY 2015 to $3.8 billion in FY 2024.

That’s a compound annual growth rate of 4.8%.

I like to see mid-single-digit (or better) top-line growth out of a mature company such as this, and A. O. Smith clearly made good on that.

Meanwhile, the company grew its earnings per share from $1.58 to $3.63 over this period, which is a CAGR of 9.7%.

Very solid EPS growth out of A. O. Smith, especially considering its size and age.

A combination of margin expansion and share buybacks helped to drive this excess bottom-line growth.

Regarding the latter, the outstanding share count has been reduced by nearly 20% over the last decade.

Growth has been a bit lumpy, as construction can be cyclical, but the longer-term picture out of A. O. Smith is quite impressive.

Looking forward, CFRA believes that A. O. Smith will compound its EPS at an annual rate of 4% over the next three years.

CFRA cites China weakness, tariff pressures, and higher steel costs as reasons to be somewhat cautious over the near term.

However, CFRA appears to be enthusiastic about the company’s long-term prospects: “[A. O. Smith] is well positioned for growth in emerging markets, particularly India, nonresidential/replacement markets, and its water treatment segment due to the increasing need for filtration systems. New product launches (Adapt SC tankless, HomeShield PFAS filter) support our view.”

These are all secular stories, eclipsing short-term concerns over costs or specific market weakness.

CFRA then adds: “Additionally, its underleveraged balance sheet provides flexibility for accretive M&A in higher-growth water technology platforms.”

I think this is a key differentiator for A. O. Smith.

Its acquisitive nature, allowed for by its financial strength, has broadened its portfolio in order to diversify away from heaters/boilers and address shortages across the marketplace.

A perfect example of this is the 2023 acquisition of Water Tec, an Arizona-based water treatment company.

A. O. Smith is increasingly becoming a one-stop shop for water solutions.

While CFRA may be proven right over the near term, A. O. Smith’s longer-term growth trajectory seems likely to revert to the mean, which would imply high-single-digit EPS growth.

With the payout ratio being as low as it is, that opens up the dividend to potentially grow at an even faster rate.

Again, the yield isn’t super high, nor would I expect it to be out of a Dividend Aristocrat involved in secular growth around water, but the combination of yield and dividend growth should add up to a low-double-digit annualized total return (which jibes with the stock’s ~10% CAGR, including reinvested dividends, over the last decade).

That’s very respectable.

Financial Position

Moving over to the balance sheet, A. O. Smith has a spectacular financial position.

The long-term debt/equity ratio is 0.1, while the interest coverage ratio is over 100.

Furthermore, the company has a net cash position.

This magnificent balance sheet, which speaks on what CFRA mentioned earlier, is present in spite of the company’s acquisitive nature, just going to show how well this business is run and how much flexibility is retains for more acquisitions in the future.

Profitability is extremely robust.

Return on equity has averaged 23.8% over the last five years, while net margin has averaged 12.1%.

The company is routinely generating high returns on capital, which is emblematic of a high-quality business earning returns well in excess of its cost of capital (i.e, creating shareholder value).

And net margin has been steadily expanding from the ~10% area a decade ago toward the ~14% mark more recently, showing the additional value of accretive acquisitions.

This might just be one of the very best pure-play opportunities in the entire water space.

And with economies of scale, brand power, an oligopolistic market structure, IP, R&D, and barriers to entry, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

The company is directly exposed to the domestic home construction industry; by extension, A. O. Smith is very much affected by interest rates and broader US economic cycles.

Input costs are volatile, and inflation has recently led to higher costs across the board.

The international footprint, although a relatively small portion of the overall company, subjects A. O. Smith to geopolitics and currency exchange rates.

A trend toward tankless water heaters may result in more sales for Chinese competitors, as A. O. Smith isn’t yet quite as entrenched and dominant in this area of the market.

The company’s expanding reach into water treatment, while promising and something I endorse, is a somewhat new and unproven area for the company.

The TAMs for A. O. Smith are not particularly large, which is why the company’s market cap is still just ~$10 billion even after 150+ years of operation and growth.

I view the overall risk profile as being fairly low for A. O. Smith, at least relative to many other business models I look at.

Yet, with the valuation being where it’s at, it seems to me like a lot of risk (and even more than normal) is being unjustifiably priced in…

Valuation

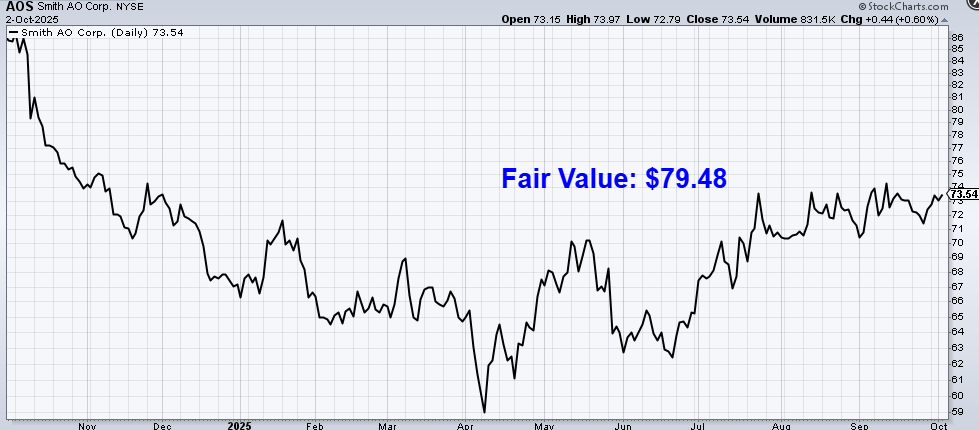

The P/E ratio on the stock is sitting at 20.3.

That’s well below its own five-year average of 24.1, and it’s also below where the broader market’s earnings multiple is at.

The cash flow multiple of 17.4, which is not high in absolute terms, is lower than its own five-year average of 18.3.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

This growth rate is at the high end of what I normally allow for, but I feel this Dividend Aristocrat earns the benefit of the doubt.

Its 10-year dividend growth rate is nearly twice this level.

Moreover, the company has comfortably compounded its EPS at a rate that easily exceeds my go-forward mark.

With the payout ratio being as low as it is, I see no reason why A. O. Smith can’t make good on high-single-digit dividend growth over the coming years, although there will almost certainly be moderate ebbs and flows along the way.

The DDM analysis gives me a fair value of $73.44.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

At worst, my viewpoint is that this stock is fairly valued, and it’s hardly criminal to pay a fair price for a high-quality Dividend Aristocrat.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates AOS as a 3-star stock, with a fair value estimate of $77.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates AOS as a 4-star “BUY”, with a 12-month target price of $88.00.

I’m on the low end this time around. Averaging the three numbers out gives us a final valuation of $79.48, which would indicate the stock is possibly 8% undervalued.

Bottom line: A. O. Smith (AOS) is a high-quality company catering to the world’s growing thirst for accessible, clean water. Water is our most precious resource, necessary for sustaining life, and I think it’s set to become the “liquid gold” of the coming century, boding well for A. O. Smith and its roster of water-related offerings. With a market-beating yield, a moderate payout ratio, double-digit dividend growth, more than 30 consecutive years of dividend increases, and the potential that shares are 8% undervalued, long-term dividend growth investors would be prudent to consider adding this Dividend Aristocrat to portfolios now.

-Jason Fieber

Note from D&I: How safe is AOS‘s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, AOS‘s dividend appears Very Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Disclosure: I’m long AOS.

{kind=link}