As someone who lived abroad for nearly a decade, I ran into many older Americans who were involuntarily living in foreign countries due to economic hardship.

They were economic refugees of a sort, unable to afford a basic life in America on Social Security alone and forced to live elsewhere.

This is really sad.

But it’s also largely preventable.

It does take some foresight, planning, patience, and discipline, but wealth in old age is almost an unavoidable outcome for those who consistently save and intelligently invest capital throughout their lives.

With the power of compounding, even small sums consistently put away can add up to significant amounts of money over the course of decades.

One of the best ways to put that money to work over time is to utilize the dividend growth investing strategy.

This is a long-term investment strategy based on buying and holding shares in world-class businesses rewarding shareholders with growing dividends.

You can find numerous examples of such businesses by pulling up the Dividend Champions, Contenders, and Challengers list.

This list has compiled data on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

These businesses are so good and so able to routinely grow profits that they can afford to steadily pay out ever-larger cash dividends to their shareholders.

And reliable, safe, growing dividend income can be the bedrock of a comfortable life.

I’d know firsthand.

I’ve been using the dividend growth investing strategy for 15 years, letting it guide me as I’ve gone about building the FIRE Fund.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

This has been enough to provide me with a comfortable life since I quit my job and retired in my early 30s, which is something my Early Retirement Blueprint details.

Now, there is one very important aspect of the dividend growth investing strategy that you should know about: valuation.

See, price is only what you pay, but value is what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Using dividend growth investing and the power of compounding to your advantage by steadily acquiring undervalued high-quality dividend growth stocks prevents a future of impoverishment in old age, setting up a comfortable life funded by growing dividend income from world-class businesses.

Of course, knowing which of these stocks may be undervalued sounds easier said than done.

Well, it’s not as difficult as you might think.

Lesson 11: Valuation, written by fellow contributor Dave Van Knapp as part of a series of “lessons” designed to teach dividend growth investing, explains how valuation works and how to go about quickly estimating the fair value of almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Marsh & McLennan Companies Inc. (MMC)

Marsh & McLennan Companies Inc. (MMC) is an American professional services firm which operates globally.

Founded in 1871, Marsh & McLennan is now a $99 billion (by market cap) solutions provider which employs approximately 90,000 people.

Marsh & McLennan has clients in 130 countries.

The company operates across two segments: Risk & Insurance Services, 63% of FY 2024 operating revenue; and Consulting, 37%.

Its main segment, Risk & Insurance Services, is anchored by the company’s position as the world’s largest insurance broker.

An insurance broker is an intermediary between clients (such as individuals or even businesses) and insurance companies, and this intermediary status takes on none of the financial risk associated with insurance.

Its brokerage business is the crown jewel of the enterprise, featuring “tollbooth” characteristics.

The brokerage maintains “sticky” customers and feeds off of recurring insurance transactions (taking a percentage of insurance premiums via a commission charge).

This is a fee-based business with visible and recurring revenue, and it sports very high returns on capital and margins, lifting the rest of Marsh & McLennan with it.

On the other hand, the rest of Marsh & McLennan is also quite solid.

The consultancy is a capital-light, asset-light business model with loyal clientele of its own, and it has the ability to scale and generate higher revenue with little incremental increases in costs.

Like the insurance side of the house, its consultancy work has a lot to do with risk management for its clients (and insurance, as we know, is all about risk management).

Marsh & McLennan has relied on this “one-two punch” across different elements of risk management to propel the company higher for years.

It’s been a success story for more than 150 years.

I see nothing to indicate that it won’t continue to work extremely well for the decades to come, which should translate into higher revenue, profit, and dividends.

Dividend Growth, Growth Rate, Payout Ratio and Yield

Already, Marsh & McLennan has increased its dividend for 16 consecutive years.

Its 10-year dividend growth rate is an impressive 11.1%.

The last several years actually featured dividend growth above this level – typically in the 15% area – but the most recent dividend raise did come in at an on-trend 10.4%.

Either way, Marsh & McLennan has been a lock for double-digit dividend growth almost from the start.

And you’re pairing that with the stock’s starting yield of 1.8%.

This market-beating yield isn’t bad at all when judged against the higher dividend growth rate (a dividend growth rate this high is often traded off against an even lower yield than this).

Notably, this yield is also 40 basis points higher than its own five-year average.

And it remains a very secure dividend, backed by a payout ratio of 43.2%.

To me, this is just a solid dividend profile right across the board.

Good yield, great growth, clear commitment from management to the dividend, and soundness in the level of the payout.

There’s almost nothing to complain about, unless one is really hungry for yield.

Revenue and Earnings Growth

As much as that may be the case, though, this dividend profile is mostly based on what’s already happened in the past.

However, investors must always be thinking about what’s likely to happen in the future, as the capital of today gets put on the line and risked for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be instrumental for the valuation process.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this manner should give us enough details to confidently judge where the business could be going from here.

Marsh & McLennan moved its revenue from $12.9 billion in FY 2015 to $24.5 billion in FY 2024.

That’s a compound annual growth rate of 7.4%.

I’m usually looking for a mid-single-digit (or better) top-line growth rate out of a mature firm like this, but Marsh & McLennan exceeds expectations.

It should be said that Marsh & McLennan’s acquisitive nature, which brought a number of smaller businesses into the fold, has had a helping hand in driving absolute size and growth for the firm.

Meanwhile, earnings per share grew from $2.98 to $8.18 over this period, which is a CAGR of 11.9%.

Boy, that’s good stuff.

I like what I see.

Excess bottom-line growth was helped by accretive acquisitions, margin expansion, and buybacks.

Regarding that last point, the outstanding share count has been reduced by about 7% over the last decade.

We can now see that 11%+ dividend growth has been coming from very similar EPS growth, proving out just how well management has been captaining the ship.

I’d also like to point out that EPS growth has been secular and relentless over the last 10 years, showing almost no abatement from a steady march upward every year.

This speaks on what I noted earlier, about how Marsh & McLennan operates something akin to a tollbooth with its brokerage.

Looking forward, CFRA is calling for a 9% CAGR for Marsh & McLennan’s EPS over the next three years.

CFRA cites the crown jewel of the firm as something to be optimistic about, with an asymmetrical risk-reward profile: “We believe this global provider of advice and solutions in the risk, strategy, and human capital markets will benefit from increased demand and improved terms for risk management and transfer services, but without the exposure to claim costs that insurance underwriters face.”

That’s really the crux of it.

Marsh & McLennan captures the upside of rising insurance demand, but it doesn’t face the downside risk of claims.

However, CFRA’s enthusiasm is somewhat tempered by the consultancy side of the house, noting that “…topline growth at [Marsh & McLennan] in coming periods is projected to lag that of most peers (particularly the “pure-play” insurance brokers)…”

Indeed, to this point, whereas the company’s Risk & Insurance Services produced nearly 10% YOY revenue growth last year, Consulting did just mid-single-digit YOY revenue growth.

This diversified setup, with its smaller business acting as a laggard right now, will benefit the combined firm when insurance is experiencing problems, but it’s been a headwind during a favorable hard market for insurance over the last few years.

To the company’s credit, it has spent a number of years tilting toward insurance (and, consequently, away from consulting).

The acquisition of U.K.-based insurance broker Jardine Lloyd Thompson Group PLC for ~$5.6 billion in 2019, along with the 2024 acquisition of McGriff Insurance Services, LLC for ~$7.8 billion, are prime examples of Marsh & McLennan’s leaning into insurance.

Overall, balancing things out, I don’t have a problem with CFRA’s near-term forecast, although I’d be keen to give Marsh & McLennan the benefit of the doubt and assume something closer to its historical growth rate (especially with the favorable portfolio churn playing out).

Essentially, I view the company as likely to generate more LDD EPS growth over the coming years, which sets the dividend up for more LDD growth of its own.

Putting that on top of the near-2% starting yield paints a nice picture – one where investors could be getting a low-teens annualized total return out of the stock over time.

Seeing as how this stock has generated a 15%+ CAGR (including reinvested dividends) over the last decade, there’s nothing herculean about that type of expectation.

Again, unless one is focused almost exclusively on yield, this should easily satisfy most investors, especially those who are younger and capable of letting compounding do its magic over time.

Financial Position

Moving over to the balance sheet, Marsh & McLennan has a good financial position.

The long-term debt/equity ratio is 1.4, while the interest coverage ratio is almost 9.

These are not excellent numbers, but the acquisitive nature of the company explains the leverage.

The company ended last fiscal year with roughly $6 billion in long-term debt, which is relatively immaterial for a firm of this size.

I wouldn’t mind seeing a healthier balance sheet, but I’m also not particularly concerned here.

Profitability for the firm is excellent.

Return on equity has averaged 29.7% over the last five years, while net margin has averaged 15.1%.

Although the balance sheet lends a hand to ROE, even ROIC is often in a mid-teens area.

Marsh & McLennan is clearly very high returns on capital, which is a hallmark of a high-quality company.

Overall, I see a fundamentally strong business with a lot going for it.

And with economies of scale, barriers to entry, “sticky” customers, and brand recognition in the industry, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

In particular, both insurance and consulting are extremely competitive, although Marsh & McLennan’s scale and brand power help to mitigate some of the competitive pressures.

The insurance industry is mature, limiting the company’s growth potential in its largest and most profitable segment.

Some of Marsh and McLennan’s growth is reliant on price increases across insurance, which is outside of the company’s control.

Being global, there is exposure to geopolitics and currency exchange rates here.

The law of large numbers may start to catch up to the company, as it’s already the largest firm in its industry (which may limit its growth profile relative to smaller firms).

I don’t see a high risk profile for this company, which makes sense for what is a risk manager.

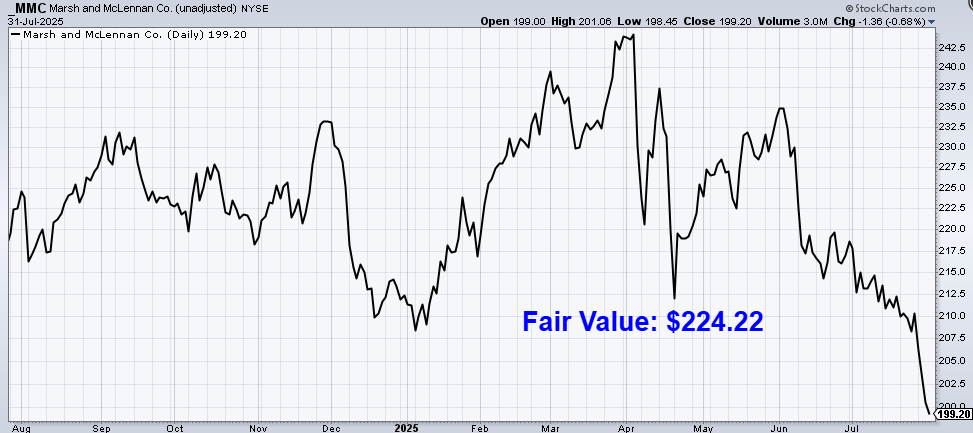

I also don’t see a lot of risk relating to the valuation, which has compressed quite a bit after the stock’s near-20% slide since April…

Valuation

The P/E ratio of 24.8 is not egregious for a company with secular double-digit bottom-line growth.

This is well below its own five-year average of 27.8.

The cash flow multiple of 18.1, which is undemanding, is also under its own five-year average of 19.2.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 10-year dividend growth rate of 11%, and a long-term dividend growth rate of 8%.

I’m extrapolating out the 10-year dividend growth rate into the next decade, which seems like a very reasonable thing to do.

The firm is growing at a LDD rate, and it’s expected to keep that up (more or less).

Also, the most recent dividend increase was very close to this mark.

All signs are pointing to Marsh & McLennan continuing to compound its EPS and dividend at 10%+ rates, respectively.

However, it would be normal to assume some eventual slowdown, which I foresee being in a HSD range.

For the growth and quality that Marsh & McLennan exudes, none of this is even close to unrealistic.

The DDM analysis gives me a fair value of $250.66.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I think the stock looked pretty fairly priced at April highs near $250, but the recent slide to the ~$200 level may have created some nice undervaluation.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates MMC as a 2-star stock, with a fair value estimate of $192.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates MMC as a 3-star “HOLD”, with a 12-month target price of $230.00.

I came out on the high side, which surprises me. Averaging the three numbers out gives us a final valuation of $224.22, which would indicate the stock is possibly 10% undervalued.

Bottom line: Marsh & McLennan Companies Inc. (MMC) is a high-quality firm, deftly balancing a terrific insurance brokerage business with a high-margin consultancy business. It’s generating high returns on capital, fat margins, and consistent growth through a “tollbooth” type of operation. With a market-beating yield, double-digit dividend growth, a moderate payout ratio, more than 15 consecutive years of dividend increases, and the potential that shares are 10% undervalued, long-term dividend growth investors looking to invest in a world-class insurance brokerage have a good shot on goal right now.

-Jason Fieber

Note from D&I: How safe is MMC’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 80. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, MMC’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Disclosure: I have no position in MMC.

{kind=link}